Retirement offers the time and perspective to think about what truly matters and what should endure. Beyond managing accounts or updating documents, legacy and estate planning in retirement is about shaping how your values, generosity, and lessons continue to make an impact—today and for years to come.

A living legacy brings those elements together. It’s how your beliefs and priorities show up in daily life, in relationships, and in how wealth is stewarded for others. The choices you make now can lighten future burdens, express your intentions clearly, and ensure your story continues long after.

In this guide, you’ll explore how to:

- Define what a “living legacy” really means—and why it matters.

- Connect personal values to the structure of your estate and giving plan.

- Use tax-efficient tools like required minimum distributions (RMDs), qualified charitable distributions (QCDs), and donor-advised funds (DAFs).

- Start meaningful family conversations that reduce confusion later.

- Keep your plans current through simple annual reviews.

Together, these steps can help you shape a legacy that’s both lived now and prepared for tomorrow. Let’s begin by clarifying what “living legacy” really means—and how it fits within a broader legacy and estate planning strategy.

What “Living Legacy” Really Means

Legacy is often framed as a set of documents—a will, a trust, a beneficiary form. Those are important, but they don’t capture the full picture. A living legacy also includes the mentoring call that becomes a monthly ritual, the volunteer work that gives your week meaning, or the steady gifts that keep a local program’s lights on.

A living legacy is character in action. It’s also deeply practical. Clear medical preferences, coordinated beneficiary designations, and a plan for who does what if something happens are as much a gift as any check.

Longevity trends make this even more relevant. According to federal data, life expectancy at age 65 rose in 2023 to an average of 19.5 additional years—about 18.2 for men and 20.7 for women. That means many retirees are planning for decades of purpose, not a brief final chapter.The key question isn’t just what to do—it’s what to do first.

Start With Meaning, Then Add Structure

Good plans begin with plain words. Write down the values that deserve to keep traveling—generosity, stewardship, curiosity, faith, care for the natural world—and the people or causes that should feel those values most directly. Capture one or two stories that explain why. That narrative will guide choices far better than a spreadsheet ever could.

Next, layer in the structural elements that make those intentions portable:

- Required minimum distributions (RMDs): For most retirees, tax-deferred accounts require minimum annual withdrawals starting at age 73. Coordinating these withdrawals with family support or charitable giving can turn a compliance step into a legacy habit. Learn more about RMDs.

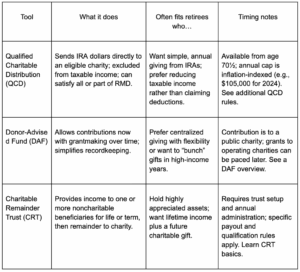

- Qualified charitable distributions (QCDs): If you’re 70½ or older, you can direct a QCD from your IRA to an eligible charity. When handled correctly, the amount is excluded from taxable income and can satisfy all or part of that year’s RMD. The annual cap is inflation-indexed ($105,000 for 2024). Get more details on QCDs.

- Donor-advised funds (DAFs): These allow you to make a charitable contribution, take an immediate deduction (subject to IRS limits), and recommend grants over time. Donor-advised funds can simplify giving and recordkeeping, but have specific rules.

- Charitable remainder trusts (CRTs): These irrevocable trusts can provide income during your lifetime and direct remaining assets to charity afterward. They suit retirees with highly appreciated assets who want to balance income and giving. Learn about CRT basics.

The appropriate structures for you depend on your temperament, tax picture, and goals.

Conversations That Carry a Legacy Forward

A plan not communicated is a plan at risk. Share the “what,” the “why,” and the “how” with the people who may one day carry it out. One conversation can create alignment and accomplish more than a dozen forms and documents. It can be difficult to know where to begin, so here are two important areas you might consider covering first.

- Start with medical preferences. Advance care planning—choosing a health care proxy, documenting wishes, and sharing them—helps reduce uncertainty when decisions are hardest. Explore these advance care planning resources and discuss them with your financial professional.

- Clarify survivor benefits. If a spouse, child, or dependent parent might rely on survivor benefits, make sure they know what’s available and how to begin drawing benefits when the time comes. Social Security outlines eligibility, payment basics, and next steps for survivors. Learn about Social Security survivor benefits on the official SSA.gov website.

Legacy and estate planning topics can feel heavy. Framing them as acts of care—another way of protecting dignity and easing burdens—often helps families approach them with more openness and less friction.

Living the Legacy (Not Just Documenting It)

A living legacy isn’t built in grand gestures; it’s shaped by the ordinary pace of life. It’s visible in who gets time, what gets funded, and which habits are repeated until they become part of the family’s culture and identity. Consider three simple, enduring ways to shape a living legacy and keep values in motion:

- Practice presence: Mentor a younger neighbor or relative on a regular basis, like coffee and questions on the first Monday of each month.

- Practice generosity: Tie giving to rhythms you already follow, such as your RMD month, birthday month, or a shared family value or interest like parks, literacy, or food security.

- Practice storytelling: Record short voice memos about lessons learned, favorite memories, or milestones. Collect and label photos with context, not just names.

None of these activities necessarily requires large sums of time or money. Yet, all of them shape how people remember what mattered to you—and how they can carry it forward.

A Quick Guide to Common Giving Tools (and Who They Fit)

The table below summarizes three frequently used charitable tools. It’s not exhaustive and doesn’t replace personalized advice, but it can help you explore ideas to discuss with your financial professional.

Why this matters: Choosing a structure that matches intent can make giving easier to sustain during life and more likely to continue after your passing.

A Gentle Tune-Up for Existing Legacy and Estate Plans

Even well-built plans drift if life changes and documents don’t. A routine yearly checkup—and updates after major events—can keep your living legacy aligned with reality:

- Beneficiaries and titling: Confirm that beneficiary designations on retirement accounts and insurance policies match your intentions. These designations typically override wills and trusts.

- Giving calendar: Schedule reminders for QCDs or donor-advised fund grants to keep generosity consistent.

- Medical documents: Revisit your health care proxy and directives after major family events, and ensure trusted individuals know where documents are stored.

This is the “maintenance mode” of legacy and estate planning: routine reviews and periodic updates that can be surprisingly effective at preventing future confusion.

When Family Is Part of the Legacy Plan

Blended families, special-needs dependents, family businesses, or shared properties can add layers to a plan. Don’t let that complexity cause delay—address it clearly.

- Explain in writing why gifts or provisions are structured as they are.

- Clarify roles (executor, trustee, power of attorney, health care proxy) and name alternates.

- Store documents, contacts, and account instructions in one organized place.

- If survivor income is relevant, make sure loved ones understand how to begin with Social Security survivor benefits.

These steps won’t eliminate every question, but they significantly reduce confusion and conflict.

Frequently Asked Questions About Living Legacies & Legacy Planning

What’s the difference between a “living legacy” and traditional estate planning? A living legacy is the day-to-day expression of values—mentoring, volunteering, steady giving, and clear communication with loved ones—while estate planning supplies the documents and designations that keep those values moving when you’re gone. Both matter. For example, beneficiary forms on retirement accounts often control who receives those assets, regardless of what a will says; keeping beneficiary designations aligned with your intentions is essential.

How do required minimum distributions (RMDs) fit into a living legacy? RMDs are mandatory withdrawals from most tax-deferred retirement accounts starting at age 73 for many retirees. Coordinating these withdrawals with gifts to family or charity can turn a compliance task into a legacy habit—especially if cash flow is tight earlier in the year. The IRS explains timing and calculation rules for required minimum distributions, including the “required beginning date” and year-end deadlines.

I already give to charity. What’s the simplest way to align that with retirement tax rules?

If you’re age 70½ or older and give regularly, you might consider a qualified charitable distribution (QCD)—a direct IRA-to-charity transfer that can be excluded from taxable income when executed correctly and can count toward that year’s RMD. The annual QCD cap is inflation-indexed (for example, $105,000 for 2024). You’ll find the current limits and mechanics under qualified charitable distributions.

What conversations can reduce confusion for my family later? Two stand out. First, talk through advance care planning—who will make medical decisions if you can’t, what your preferences are, and where documents live. The National Institute on Aging offers plain-language guides to advance directives and health care proxies. Second, if a spouse or dependents might rely on Social Security after your death, share basics from survivor benefits so loved ones know eligibility and where to begin.

How often should I review my legacy “mechanics” (beneficiaries, titling, documents)? A quick check once a year—and after any major life event—is usually enough. Confirm that beneficiary designations match your intentions, account titling supports your plan, and health-care documents still reflect your wishes. Small, regular updates prevent the big surprises.

Is there a way to keep giving consistently without feeling administrative overload? Yes. Many retirees anchor generosity to calendar cues—RMD month, birthday month, or twice-yearly “grant windows.” For some, a DAF simplifies record-keeping and scheduling (DAF overview). For others, QCDs keep gifts steady while helping manage taxable income (QCD rules). Choose the rhythm that’s easiest to sustain.

What’s the most underrated element of a living legacy? The story that explains the plan. A brief “values letter” or ethical will turns numbers into meaning, guiding loved ones when decisions are hard. Pair that narrative with the practical pieces above—RMD awareness, appropriate charitable tools, clear medical directives, and accurate beneficiary forms—and the result is a legacy people can feel today and carry forward tomorrow.

The Heart of the Matter

A living legacy is not a grand gesture reserved for the end of life. It is the quiet accumulation of everyday choices and steady practices. It’s how you spend your time, express generosity, communicate decisions, and document wishes so they can continue when you no longer can.

The technical pieces—required withdrawals, QCD limits, DAF rules, CRT administration, medical directives, and survivor benefits—support that vision. But the heart of a living legacy is deeper: the values you want to last and the people and causes you entrust to carry them forward.

If you’d like to explore how these ideas can support your unique legacy and estate planning goals, reach out to the office to schedule a meeting with your financial professional. Together, we can design a legacy that reflects your life now—and continues to make an impact for years to come.

*Generally, a donor advised fund is a separately identified fund or account that is maintained and operated by a section 501(c)(3) organization, which is called a sponsoring organization. Each account is composed of contributions made by individual donors. Once the donor makes the contribution, the organization has legal control over it. However, the donor, or the donor’s representative, retains advisory privileges with respect to the distribution of funds and the investment of assets in the account. Donors take a tax deduction for all contributions at the time they are made, even though the money may not be dispersed to a charity until much later.

** The use of trusts involves a complex web of tax rules and regulations. You should consider the counsel of an experienced estate planning professional before implementing such strategies.